The Price of Loyalty

Today's featured startup will help you identify your best and most loyal customers.

Project Overview

Ansa aims to help merchants "unleash the potential of their best customers" in two key ways:

Identifying customers who have the potential to become loyal.

Providing a tool to encourage repeat purchases from these customers.

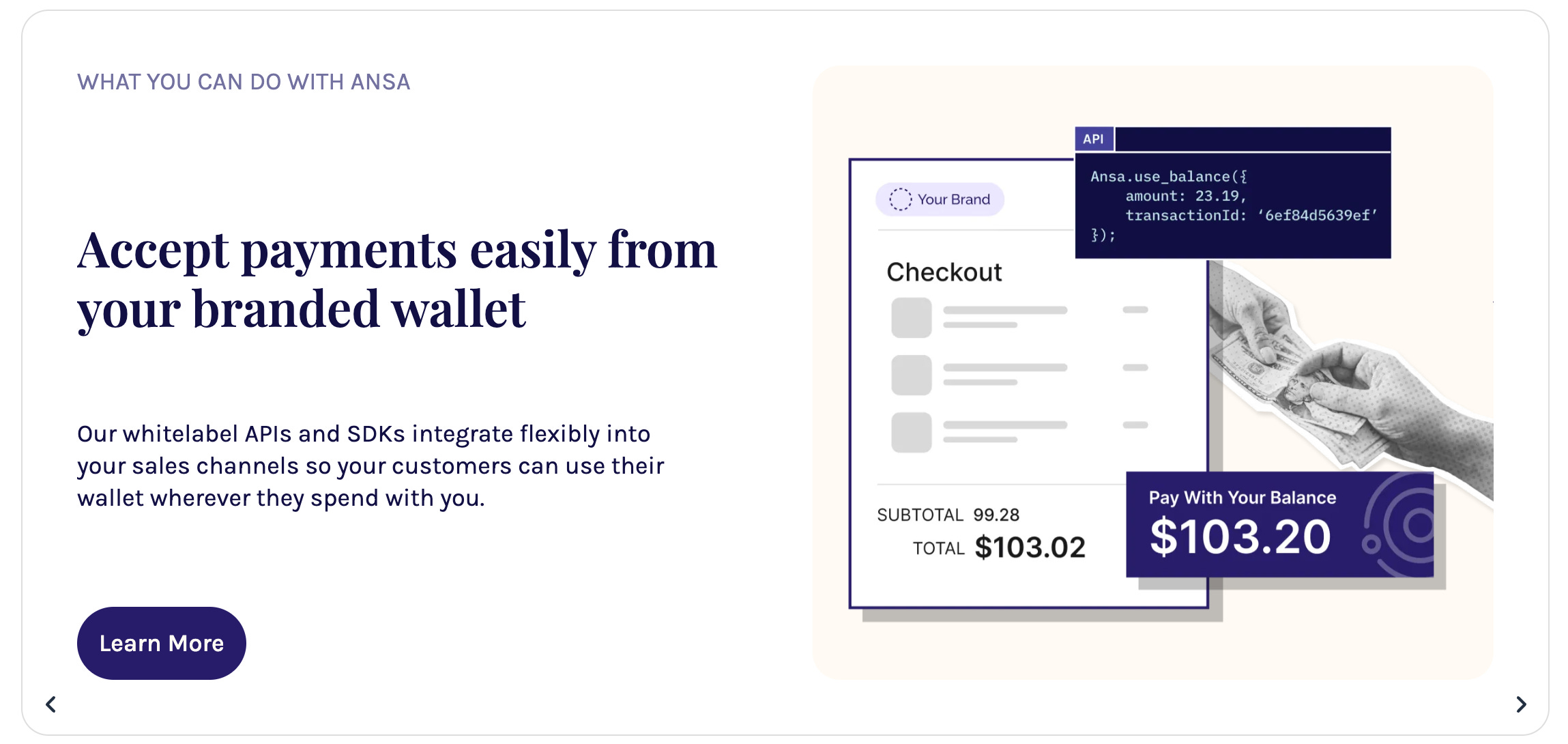

To achieve this, Ansa enables merchants to create a branded digital wallet that integrates with their store. Customers can then use the wallet to pay with funds they deposit themselves or receive as rewards from the merchant.

Only customers who plan to shop regularly at a store are likely to set up and fund a wallet, which naturally filters out potential loyal buyers. And if a customer has money sitting in a store-linked wallet, they are more inclined to spend it. This allows merchants to send targeted offers, encouraging purchases and keeping the cycle going by rewarding further transactions.

Ansa provides full API access, allowing merchants to embed wallet top-up and payment options anywhere—on their website, in their app, or any other sales channel that supports API calls.

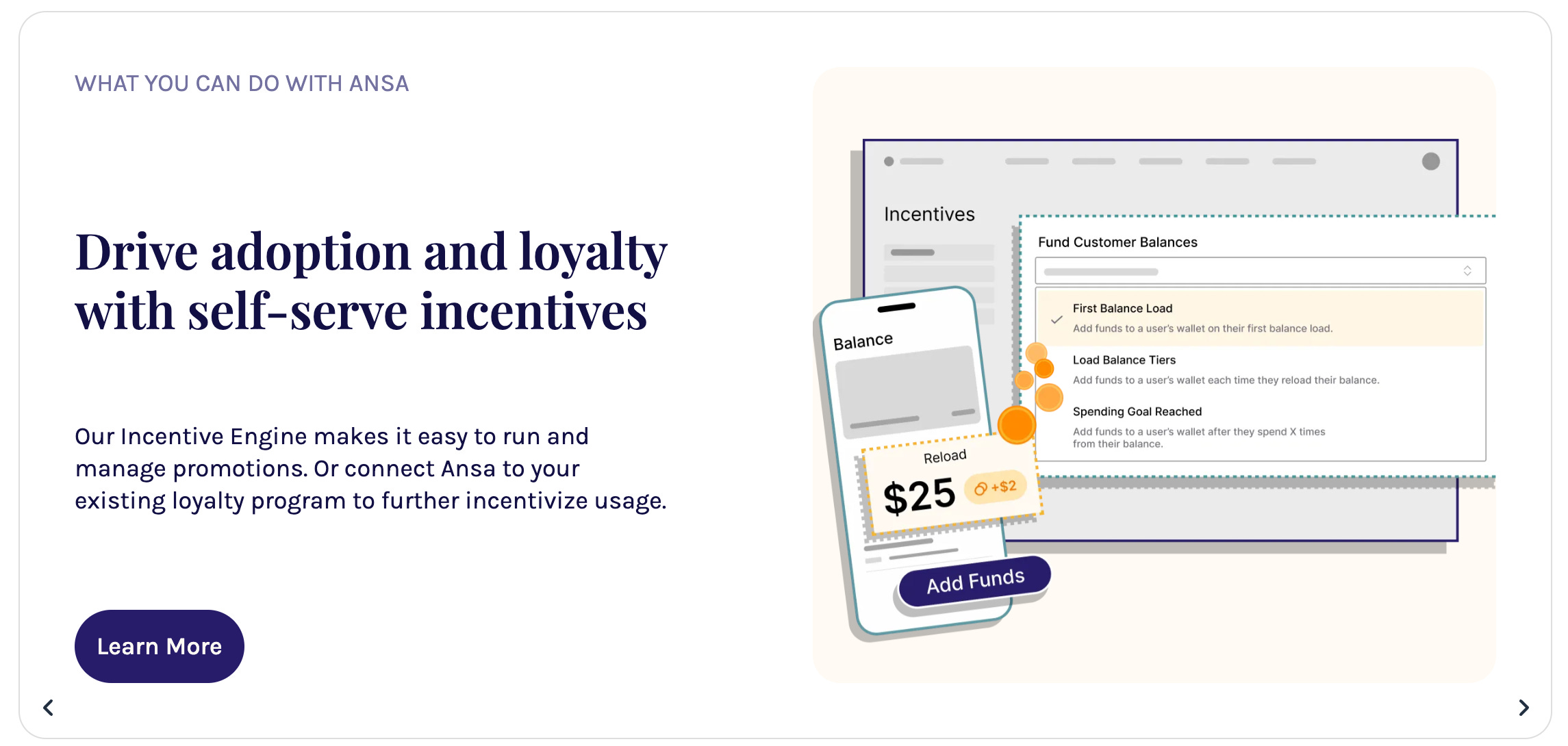

There is also an API for automating reward distribution, making it easy to create new loyalty systems or integrate with existing ones. For instance, a merchant could simply double the rewards in their current loyalty program for wallet users.

The platform tracks all wallet activity and presents it in detailed reports, helping merchants analyze the impact of promotions, rewards, and wallet usage to increase purchase frequency and order size.

One challenge is that wallet transactions must be accounted for in financial reports, adding complexity for accountants. Fortunately, Ansa includes a tool that automates financial report integration, simplifying bookkeeping.

Ansa's initial focus is on coffee shops and fast-food restaurants, where customers frequently make small-ticket purchases. One coffee shop using the platform increased its transaction volume by 30% and revenue by 26%—with the gap explained by reward spending.

Now, Ansa is expanding into marketplaces, encouraging them to offer digital wallets to buyers. While success stories in this sector aren’t yet highlighted on their website, the potential is clear.

Founded in 2022, Ansa then launched in early 2023, securing $5.4 million in initial funding. It has since experienced rapid growth, with the number of wallets on the platform doubling in Q1 2024. This momentum led to a second funding round of $14 million.

What's the Gist?

The rise of digital wallets feels similar to the early app boom when every business rushed to launch a mobile app to stay visible on users' screens. That strategy worked then and continues to be a key marketing tool today.

Wallets function in a similar way—once a customer deposits money, they are psychologically nudged to return and spend it. And merchants can keep reinforcing this behavior by adding more rewards.

Some businesses have already adopted branded wallets, but this trend could soon explode, just like mobile apps did. If that happens, platforms like Ansa, which simplify wallet creation for merchants, will become highly sought-after.

As I write this, I’m sitting in a café where I last visited over a year ago. Back then, they didn’t have digital wallets. Now, the cashier asks every customer, "Will you pay with the app? Use or accumulate rewards?"—a clear sign of growing adoption.

Beyond marketing benefits, merchants have another major incentive to adopt digital wallets—cutting payment processing fees.

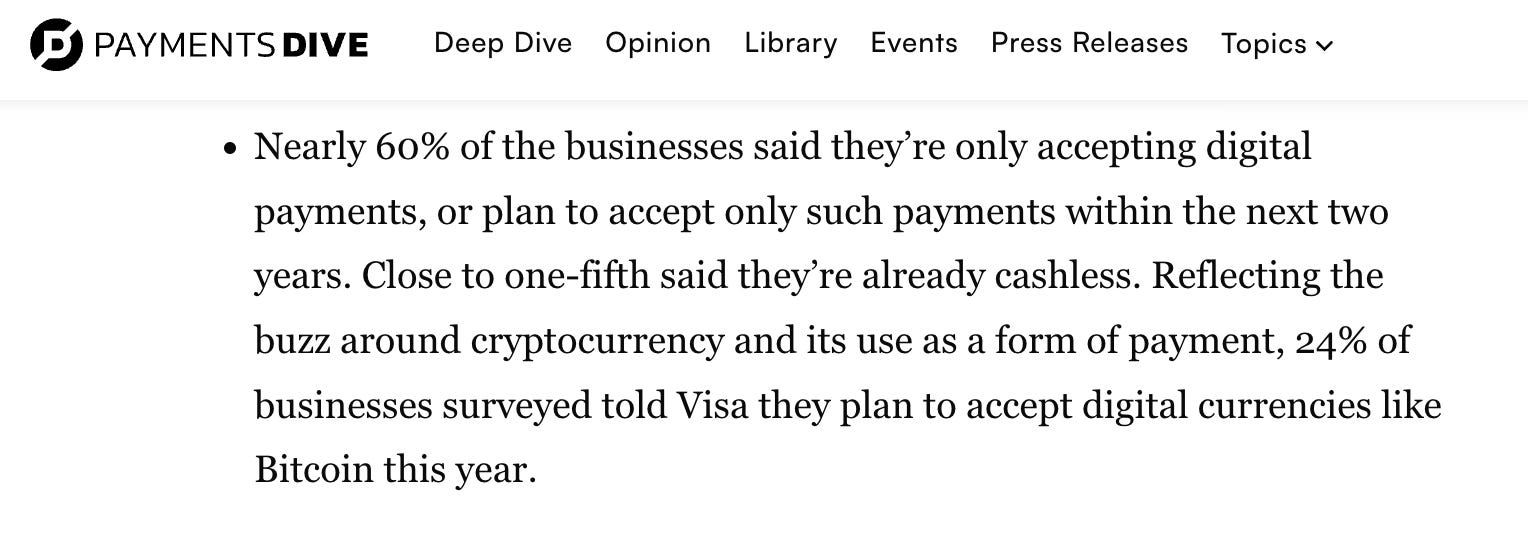

Card payments dominate retail transactions, especially in developed countries. In the U.S., 60% of retail purchases are made via cards. But merchants pay steep fees to card networks and payment processors—totaling a staggering $138 billion annually in the U.S. alone, making it the second-largest expense after employee salaries.

For small transactions, these fees are even more painful. A $4 coffee, for example, might incur a 12.5% processing fee. By shifting customers to digital wallets, merchants can significantly reduce these costs, as customers tend to preload wallets with larger amounts. Even with Ansa taking a cut, it’s still cheaper than card fees.

Key Takeaways

The smart move? Build a platform like Ansa while the digital wallet boom is still in its early stages.

If you assume that every merchant already offers digital wallets, you’re likely experiencing a tech bias—perhaps because you live in a tech-forward city or frequent innovative businesses. But 80–90% of any market consists of late adopters, and entire regions or countries still lag behind in technology adoption.

This reminds me of t Durable, a Canadian startup that launched a website builder for small businesses. Despite websites being a long-standing necessity, Durable powered 6 million new sites in its first year. Clearly, demand still exists.

Durable later raised $20.25 million in funding.

I believe digital wallets could see an even bigger boom. Now is the time to enter this space—especially with a successful model like Ansa to follow.

Company info:

Ansa

Website: https://www.ansa.dev/

Last funding round: $14 million, 30.04.2024

Total funds raised: $19.4 million after 2 rounds